BNPPRE Dashboards

The BNP Paribas Real Estate Dashboards offer us a wide range of opportunities to present real estate markets digitally and interactively. Be it at your desk or when out and about, their responsive layout enables you to view, analyse and discuss the latest market developments in different asset classes on your smartphone, tablet, PC or laptop. What’s more, the integrated filter function allows you to clearly view and compare large amounts of data at a glance. Why open a multitude of individual files or carry around pages upon pages of documents when you can quickly access an up-to-date market or location overview with just a tap or a click?

Office market key figures

Office market Q2 2026

At the half-year mark, Germany’s key office markets of Berlin, Düsseldorf, Essen, Frankfurt, Hamburg, Cologne, Leipzig and Munich recorded a take-up of 1.3 million m². Overall, the market is moving sideways. In view of the persistently weak economic momentum and the additional pressures on the wider environment since the outbreak of the Iran war, matching the previous year’s level should be regarded as a success. Meanwhile, the differentiation of the office markets continues to advance, with demand clearly focused on premium, or at least modern, space in the best micro locations. Looking at individual cities, many markets are demonstrating resilience and showing intact underlying momentum. Supported by significant large-scale deals, take-up in Berlin, Düsseldorf, Frankfurt and Munich has recently even increased. Greater confidence, planning certainty and deregulation should provide the German economy with some tailwind towards the end of the year, which would also have a positive impact on office take-up. For the year as a whole, a result slightly above the previous year’s level therefore appears entirely realistic.

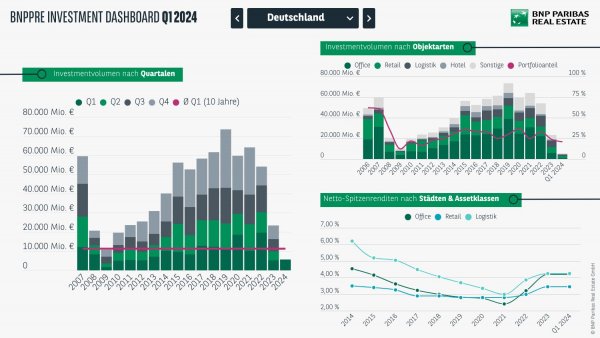

Investment market key figures

Commercial investment market Q2 2026

The German commercial investment market recorded a total transaction volume of around €12.3 billion in the first half of 2026, representing an 8% increase in turnover. With more than 700 transactions completed, it was the strongest first half-year in terms of deal momentum since 2022. A buoyant opening quarter, during which approximately €6.9 billion was invested, was followed by a second quarter in which investment activity slowed markedly (€5.4 billion). Refinancing considerations, more cautious assumptions regarding occupier markets and higher risk premia prompted a reassessment of negotiations in several asset classes. This reduced momentum, but was necessary. After all, the market will not recover on hopes of lower interest rates alone, but through pricing that realistically reflects financing conditions, rental prospects and asset complexity. Over the coming months, however, the investment market environment is likely to brighten gradually. Although geopolitical uncertainty will remain an overarching issue and economic momentum is expected to remain disappointing for the time being, the path ahead for market participants has now become more clearly defined and more predictable, both with regard to capital market developments and the real economy.

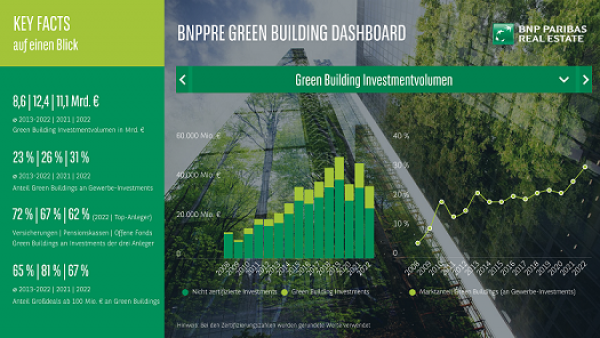

Green Building Dashboard

The share of certified green buildings within the commercial investment volume (excluding portfolios) remains at a very high level, even in a challenging market environment. After the top figure of just under 31% in 2022, around 27% was achieved in 2023. This is the second-highest share in the last 10 years and confirms the importance of green investments. While the EU Taxonomy mainly concerned companies in the real estate sector that wanted to place funds on the capital market, it is now affecting more and more market participants. Accordingly, sustainability regulations are becoming increasingly important for investors and buyers across the board, while at the same time occupiers (tenants and leaseholders) must now also take taxonomy criteria into account in their corporate governance. Against this backdrop, proactive management will remain the order of the day in 2024.

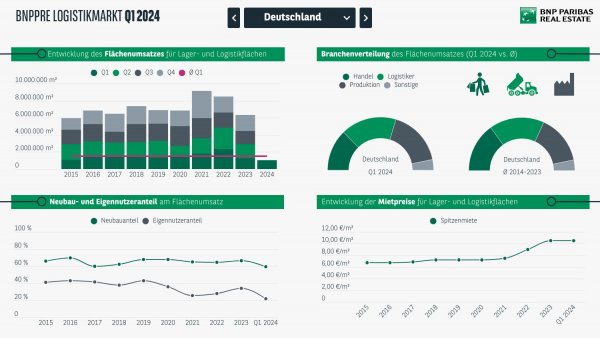

Logistics market key figures

Logistics market Q2 2026

The nationwide warehouse and logistics market continues its impressive path to growth and closes H1 with take-up of 3.3 million m². This result is 23% higher than in the previous year and also slightly above the ten-year average (+4%). The 2nd quarter was able to increase by almost 16% compared to the first three months of the year. This result is all the more remarkable in view of the economic and geopolitical conditions, which were further burdened in particular by the Iran war and the conflict over the Strait of Hormuz. Overall, there was brisk market activity with a high number of contracts, with significantly more major deals of 20,000 m² or more than in previous years. Logistics service providers remain by far the largest demand group, with a market share of 44% and numerous large-scale contracts. The trend that has been going on for some time now that companies in the e-commerce sector are increasingly commissioning logistics service providers to handle their business is continuing. This is especially true for companies from the Asian region, especially from China, but also for other online retailers such as Amazon, which are expanding more strongly again. While take-up in the top logistics markets (Berlin, Düsseldorf, Frankfurt, Hamburg, Cologne, Leipzig and Munich) fell by 6% to 1.0 million m², the result outside the major logistics hubs rose by 42% to 2.3 million m².

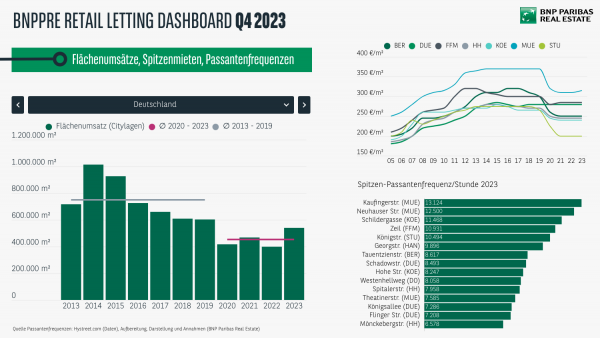

Retail market key figures

Retail market Q2 2026

In the first half of 2026, the retail market once again confirmed its currently very positive demand momentum, recording another high take-up result of around 238,000 m². Although this fell slightly short of the remarkable figure achieved in the same period last year (H1 2025: 251,000 m²; -5%), the retail sector nevertheless posted an above-average half-year result in terms of letting volume in city-centre locations (average since 2020: just over 228,000 m²). Department store re-lettings were a key driver of the strong prior-year result, generating a volume of almost 44,000 m² in the first two quarters of 2025 alone, equivalent to 17% of the total. However, around 26,000 m² has already been let in former Galeria and fashion department stores in the year to date, representing an 11% share and underlining the continued strong momentum in this segment. International retailers are also currently providing important stimulus for the German retail market: almost 15 market entries have been recorded since the beginning of the year, already exceeding the total for 2025 as a whole. These included the US activewear brand Alo Yoga on Münzstraße in Berlin and outdoor equipment specialist Yeti on Georg-Kronawitter-Platz in Munich. Overall, brands from the US accounted for 12% of deals, making them the second most active region of origin among international labels, behind Danish brands at 17% and slightly ahead of Asian players at 10%.

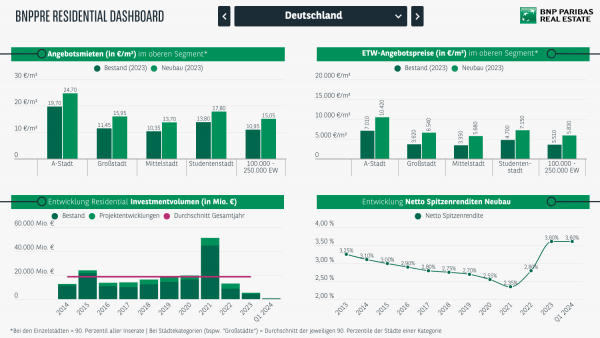

Residential market key figures

Residential Dashboard Q2 2026

The German residential investment market recorded an overall solid first half of 2026. In the first six months, around €4.4 billion was invested in residential portfolios comprising 30 units or more. This puts the result only slightly below the previous year’s level (-3%). At the same time, however, the market structure has become significantly broader: while the previous year was shaped by a small number of large-volume portfolio transactions, the number of deals has increased in the current year. Despite economic weakness and geopolitical uncertainties, the market environment remains fundamentally supportive. On the demand side, persistently strong demand for housing is coinciding with limited new-build activity, further exacerbating supply shortages, particularly in prime locations. The resulting rental growth strengthens the appeal of the asset class and underlines the role of residential property as a resilient investment haven in a volatile environment.

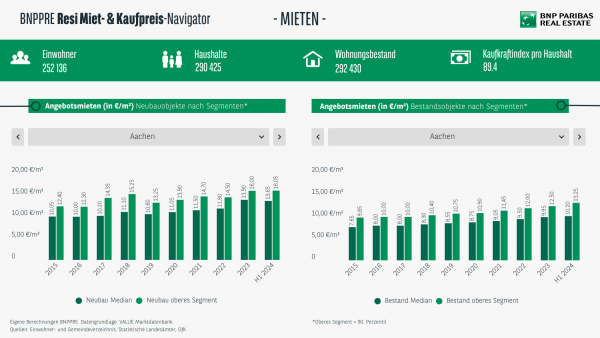

Residential rental & purchase price navigator

The residential markets of the most popular metropolises in Germany have been dominated by rising rental and purchase prices for years. But what is the situation in the rest of the country? BNPPRE investigated this question and analyzed all 108 independent cities in Germany. With the BNPPRE Residential Navigator, which is updated every six months, you can make further progress through the numerous residential markets and keep an eye on rental and purchase price developments (for condominiums) in the new builds and existing stock as well as other key figures.

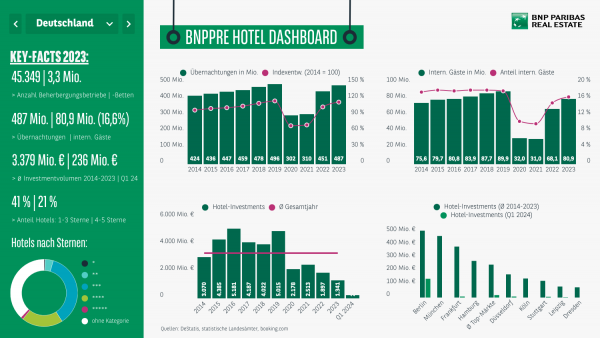

Hotel Dashboard Q4 2025

The hotel investment market can report the highest increase in investment volume compared to 2024 in an asset class comparison: The overall balance was over €1.8 billion, a remarkable 29% higher than in the previous year. It is also pleasing that the volume achieved was roughly back to the level of 2022 (just under €1.9 billion), in which the interest rate policy measures had not yet reflected to that extend in investment turnover.

The fact that both the larger and smaller city categories were able to benefit from the market revival underlines how diverse the market is at the moment: With major transactions such as the Mandarin Oriental in Munich, the Motel One Köln-Messe and the Steigenberger Hotel am Kanzleramt in Berlin, several hotel transactions with a signal effect were observed. At the same time, however, around two-thirds of the registered sales in the individual deal segment were in cities outside the A-locations, which underlines the overall broad-based demand impulses.

Hotel market key figures

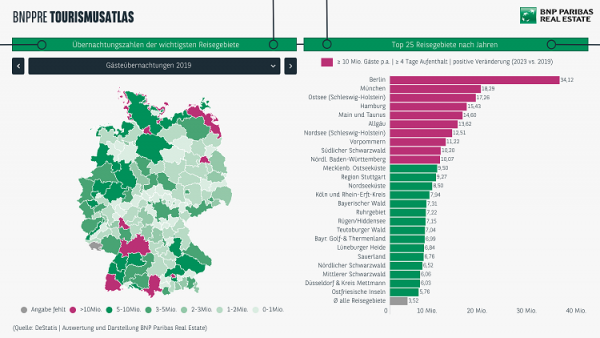

BNPPRE Tourism analyser

On the German hotel market, all key performance data indicates a sustainable recovery in tourism in Germany after the challenging COVID-19 years of 2020 and 2021. Significant increases in overnight stays by guests in accommodation establishments were already evident in 2022 (+49%) and 2023 (+61%). In 2024 around 496 million overnight stays were recorded, which not only exceeds the pre-COVID-19 figure from 2019, but also represents a new record in a long-term comparison. This reflects the resurgence in demand from city and business tourism as well as guests from abroad. Compared to the previous year, the number of overnight stays by foreign guests rose by a good 5% (85 million guests in 2024). Other key figures such as room occupancy and average prices also developed positively. By 2024, the occupancy rate had returned to a high level of just under 67% nationwide. The top 5 most popular travel destinations in 2024 are Berlin (31 million guests), Munich (20 million guests), the Baltic Sea (19 million guests), Hamburg (16 million guests) and the Main/Taunus region with 15 million guests. Furthermore, 52 million overnight stays were already registered between January and February 2025 - a strong signal for a continued positive trend in the current year.

While some dashboards are no longer up to date, they still offer an exciting insight into the various markets. Scroll through our dashboard archive here:

KEY FIGURES AND ANALYSES

ON THE GERMAN REAL ESTATE MARKET

Find out more about the latest developments in the investment, office, logistics, retail, hotel, healthcare and residential real estate markets to base your property decisions on a strong foundation of solid market information. We are happy to provide you with an extensive overview of property-related developments throughout Germany and details of the real estate markets of the largest German cities.